Zero Sum: Cities Have Little To Show For Big Spending

Authored by Jeremy Portnoy via RealClearInvestigations,

America’s largest cities are increasing their spending at almost unprecedented rates.

A RealClearInvestigations (RCI) analysis of cities with at least 500,000 residents found they cumulatively raised their per-person spending by 18 percent over the last 10 budget cycles, accounting for inflation. The only equivalents on record are the spending surges ignited by the Great Society programs of the 1960s and Franklin D. Roosevelt’s New Deal during the 1930s.

But unlike those past eras, today’s cities do not have the revenue to support their heavy spending. State and federal funding have dropped off from their record highs during the COVID-19 pandemic, and local tax hikes have not kept pace with spending. Large tax increases or reductions in city services will eventually be required to address burgeoning structural deficits, placing a burden on future generations.

The tradeoff would be easier to explain if cities were making strides to improve life for their residents. Census data, however, shows that key quality of life metrics in major cities have mostly been stagnant during the spending spree.

Each of the 38 cities in RCI’s analysis of data from the Census Bureau, FBI, Department of Housing and Urban Development, and enacted local budgets increased their spending faster than inflation over the last decade. Yet the cities that boosted their spending the most were, on average, no more or less likely to see measurable progress in reducing homelessness, lowering violent crime rates, tackling income inequality, improving rent affordability, and more. That was the case for the 33 cities led by Democrats and the five cities led by Republicans.

San Jose, California, saw its violent crime rate increase by 50 percent from 2017 to 2024, even after it doubled its police budget. The city is now proposing cuts to police spending and creating new taxes to fund its rapid budget growth in other areas. Seattle is considering shutting down its homelessness agency after huge investments failed to stop homeless rates from reaching the worst level in city history.

Christopher Thornberg, founder of the policy consulting firm Beacon Economics, isn’t surprised that big spending hasn’t produced big results. He said that cities typically don’t have the financing, policy sophistication, and regulatory oversight to meaningfully improve the economic status of their residents.

But that hasn’t stopped some cities from thinking “you can be successful just fire-hosing money across the economy,” said Thornberg, former director of the University of California, Riverside Center for Economic Forecasting and Development. “It seems sufficient to brag about the money they spent without referring to whether that spending accomplished anything.”

The Tax Gap

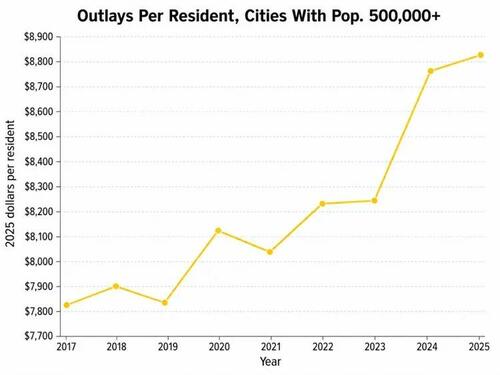

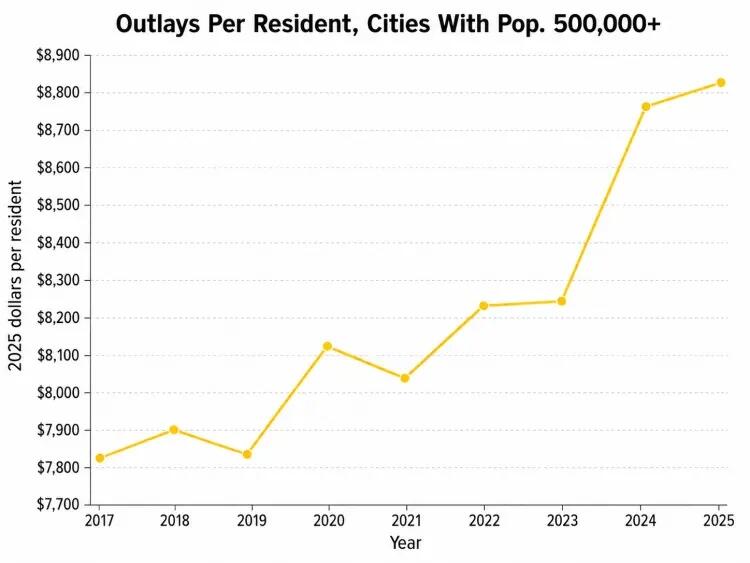

In 2016, large cities collected $6,727 of revenue per resident from local, state, and federal sources, adjusted for inflation. They spent 14 percent more than that: $7,685 per person.

RCI

By 2025, revenues had increased to $7,063 per person, but outlays had skyrocketed to $8,827. The difference of 25 percent is the largest gap on record since at least 1940.

The gap was not caused by low revenues. Cities earned record amounts of sales and property taxes last year. Instead, the deficits were driven by expanded bureaucracy, rising payrolls, overtime costs, and pension liabilities.

From 2017 to 2026, the public workforces of large cities grew faster than their populations. There were at least 12 cities that added new municipal jobs even though their populations dropped (a handful of cities do not disclose their staff headcounts). In an extreme example, Memphis added more than 1,000 public jobs even though the city lost more than 40,000 residents.

Many of those new hires work desk jobs. Census data shows large cities increased their administrative expenses—mayor’s offices, human resources departments, accountants, zoning departments, and more—by 55 percent from 2016 to 2023, accounting for inflation.

But staff headcounts at core city agencies like police and corrections departments are generally decreasing, forcing cities to spend large amounts on overtime hours to keep their communities safe with the limited staff they have available.

Crucially, RCI found only a weak statistical link between increases in a city’s property tax collection and increases in its overall spending. Cities like Phoenix and Boston that boosted their per-resident spending by 88 percent and 75 percent, respectively, were not necessarily the ones with increased property tax revenue to support their outlays.

That suggests many cities have a “build it and we will fund it” mentality, enacting policies before figuring out how to pay for them.

Previous studies have shown that outside pressures from advocates for rent affordability and labor unions influence budgets, independently of what cities can actually afford to spend. Historically, that did not cause issues because city revenues were typically higher than expenses. That went out the window after the COVID-19 pandemic, when temporary federal grants expired, and cities did not make cuts to compensate for the lost funding.

“The problem is that when governments start to spend money, they find it hard to stop spending money,” said Thornberg. “And after a year and a half of partying, you can’t get back in those old pants. You have these bloated budgets in many cities, and now they’re struggling to get their budgets back in line with a reasonable amount of revenue that can be expected.”

More Spending, More Homelessness

To illustrate these budget dynamics in action, RCI took a look at how some representative cities have responded to major issues.

Homelessness in America’s largest cities jumped by 34 percent on average from 2017 to 2024, driven partly by increased housing costs and job losses during the pandemic. RCI’s analysis found no statistically significant association between increased public welfare spending and reduced homelessness.

While Los Angeles is the poster child for getting little bang for the bucks it’s spent to combat homelessness, it is not alone. Seattle and surrounding King County were among the biggest spenders, with money pouring into the Regional Homelessness Authority. It was created by former Mayor Jenny Durkan in 2019 to “significantly decrease the incidence of unsheltered homelessness.” Washington State has also lifted its spending on housing construction by six times since then. But homelessness in Seattle increased at a faster rate than in any other large city but one, and rent price increases were also among the nation’s highest.

It’s easy to see where things went wrong. A state audit released in April found that the Homelessness Authority overspent its $200 million annual budget by $45 million, with portions of the money completely unaccounted for or spent on administrative expenses the city never approved. The authority is also paying individual contractors close to $500,000 annually, an amount unlikely to be seen as reasonable for a salaried public servant.

To find leaders with the “lived experience” of homelessness and marginalization, the authority invited a convicted repeat sex offender to join its board in 2023. When another board member objected, alleging she had been molested by the man in the past, co-chair Shanéé Colston shouted her down. “I don’t care if they’re a sex offender!” Colston said, according to the Seattle Times. “This is an inclusive space, and we are equitable to all.”

Colston was later replaced. Seattle Mayor Katie Wilson has publicly said she’s not opposed to shutting down the authority for its failure to reduce homelessness.

Nor has Portland, another big spender on homelessness, been able to reduce its soaring rate. It created a Supportive Housing Services tax in 2020 that funded Sunstone Way, a nonprofit set up by the city that collapsed in March.

Sunstone Way’s former finance director recently alleged in a whistleblower complaint that she was barred from board meetings for trying to tell county officials about the nonprofit’s “severe cash flow pressures.” She claims that when she flagged a $210,000 overpayment to a food vendor, Sunstone Way’s CEO told her to ignore it because he had “made a deal” with the vendor, who was allegedly a personal friend.

Local auditor Jennifer McGuirk warned Portland’s Homeless Services Department in 2022 that it needed to monitor Sunstone Way’s spending more carefully after it billed the government for the payroll expenses of duplicate employees. McGuirk claims she was ignored.

Homelessness decreased in 13 of the 38 cities RCI examined, but the success stories related more to policy than spending. Detroit embraced advanced data modeling systems to share information between various nonprofits, avoiding duplicated efforts and creating a real-time list of homeless individuals rather than a single annual count like most cities conduct. Homelessness dropped by 17 percent from 2017 to 2024. Milwaukee provided free lawyers to low-income tenants facing eviction and now claims to have zero people living on the street.

“Cities that have had success in battling homelessness, it turns out, it’s not just that they’re spending money, but how they’re spending money,” Thornberg said.

Although many big cities explicitly state that their budgets are designed to reduce inequality, large cities’ Gini index—a measurement of how evenly wealth is distributed—was virtually unchanged from 2017 to 2024. So was the percentage of the population with health insurance. Poverty rates improved by 1 percent on average. Cities that increased their overall budgets at a faster rate were no more or less likely to see improvement in any of those three categories.

The 10 cities with the smallest topline budget increases since 2017 all saw their poverty rates drop or remain unchanged. Those 10 cities, including Minneapolis and Long Beach, now have an average poverty rate of 13.8 percent, lower than most of their peers.

Police Spending Up, Crime Down a Bit

Violent crime rates in large cities improved slightly from 2017 to 2024, with an average decrease of 50 violent crimes per 100,000 people. The average police budget increased slightly faster than inflation.

But again, there was no statistically significant association between spending levels and violent crime rates. Cities that increased their police budgets were just as likely to see crime rates rise as cities that decreased theirs.

The negligible improvement in crime rates is especially worrisome given that other city services are being sacrificed to fund police departments. In 2022, 40 percent of America’s largest cities said public safety needs were so high that it was difficult to balance their budgets. The burden grew even higher in the following years, as police funding increased as a percentage of total city spending in both 2024 and 2025, according to the National League of Cities.

Higher spending does not always mean more police officers. Even though budgets are up, police staffing levels dropped by roughly 7 percent from 2013 to 2023, according to the Council on Criminal Justice.

That’s unsurprising given how much difficulty police departments are having recruiting new officers. Thaddeus Johnson, a senior fellow at the Council on Criminal Justice who has been teaching at Georgia State University since 2014, said college students do not view public service as “glamorous” as they did just a few years ago. “I used to ask in every class, ‘Who wants to be a cop?’ and a quarter to half of the room would raise their hands. Since the pandemic, nobody has raised their hand in class, and I’m not exaggerating. There’s no interest among criminal justice majors in policing.”

In Phoenix, where spending and violent crime rates are both up, the police department has 650 vacancies. When the department does attract workers, they don’t always stay. Thirty percent of new recruits from 2023 to 2025 have already left.

The city can’t offer higher salaries to boost its retention rate because one-third of its police budget is spent funding future pensions for officers already on the force (payments to current retirees are funded by past years’ appropriations). Arizona’s pension investments lost most of their value during the dot-com bubble of the early 2000s, and the effects still linger.

It’s a similar situation in San Jose, where 40 percent of police recruits leave the force before they become sworn officers, compared to only 6 percent in 2017. The staffing shortages force officers to work long overtime hours, driving up payroll costs.

A San Jose city audit released this April found that one quarter of all the hours police officers worked in 2025 were overtime—twice as much as in 2015. Many overtime hours were spent on report writing by officers who never obtained the required approval from their superiors to work extra hours.

Johnson said low staff headcounts are not an excuse for rising violent crime. “If there’s a million officers on the street, crime will still happen,” he said. “It’s really about how you use those officers. What is your supervisor to officer ratio? The type of training the officers are receiving? The type of technology that’s available?”

San Jose increased its per-resident police spending by 66 percent above inflation from 2016 to 2023—far more than any other city with at least 500,000 residents. But it also saw its violent crime rate per 100,000 people increase by 50 percent from 2017 to 2024, again much more than any other large city.

The crime rate did improve significantly in 2025, but remained well above pre-pandemic levels. And while San Jose’s crime rate is not necessarily higher than other comparable cities, its rapid increase despite a spending boost highlights the challenges cities face when trying to improve quality of life through budgetary means.

There are several success stories like Dallas and San Francisco, which have seen violent crime rates improve after police budgets were increased. Others, like Boston, saw crime rates improve even though police budgets did not keep pace with inflation.

Johnson cited San Antonio as an example of efficient spending. He said the city smartly deployed its officers by assigning patrols to specific places and times when crime was more likely to occur, improving public safety without breaking the bank. San Antonio’s per-resident spending on police is lower than almost any other large city, yet its violent crime rate sank by 16 percent from 2017 to 2024.

Kicking the Budget Can Down the Road

Cities will eventually have to balance their budgets, but they may face difficulty raising taxes to do so. Katherine Loughead, a vice president at the nonprofit Tax Foundation, claimed the recent upward trend in taxation is already causing “widespread unrest” among voters.

Almost every major city has a law stating that its outlays and revenues must be equal, but that does not apply to capital spending on infrastructure and city-owned property like buildings and cars. Many cities also overestimate their revenues and underestimate their spending on paper, allowing deficits to develop.

They close the gap by issuing bonds, digging into reserve funds, selling municipal property, and ignoring obligations to fund public employees’ future pension and healthcare plans.

It’s why New York City Mayor Zohran Mamdani’s highly-touted “balanced” budget proposal for 2027 is not really balanced at all. Unable to avoid reductions to city services by taxing the rich and increasing property taxes, Mamdani escaped spending cuts by shoving pension liabilities into the future for another mayor to deal with. Fifty-four of America’s 75 largest cities did the same in 2025 with either pensions or retiree healthcare costs, according to Truth in Accounting.

Chicago is already feeling the effects of that approach. After underfunding its pensions for years, Chicago now has a pension debt larger than most state governments. More than 15 percent of its budget in 2025 was spent trying to fix it, rather than being used to support taxpayers.

This summer’s budget hearings in cities across the country will likely represent a new high-water mark in structural imbalances. If past practices prevail, rather than slash services or raise taxes, most city leaders will find clever ways to once again kick the can down the road.

Tyler Durden

Mon, 06/22/2026 - 22:35

via Associated Press

via Associated Press

via Reuters

via Reuters

via CNN

via CNN

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Recent comments