Gundlach Warns "Bagholders" Will "Lose Money" In Private Credit As BDCs Slash Asset Values, JPM Faces $500MM Loss In Biggest "Hung" Deal This Year

Add another vocal warning to the chorus singing about the dangers of private credit.

DoubleLine CEO Jeffrey Gundlach, who has been especially critical of private credit for the past year warning last November that the space “has the same trappings as subprime mortgage repackaging had back in 2006,” raised fresh concerns about financial advisers and other principals who ushered retail investors into private credit and other so-called semi-liquid funds, suggesting they’ve been motivated by high fees as much as by their clients’ interests.

“It’s clear that prospectuses talked about the gating mechanism, but I have a feeling that the financial intermediaries, not all of them of course, but enough of them, didn’t explain,” he said Wednesday on a panel at the Milken Institute Global Conference in Beverly Hills.

The products have been “kept opaque and not granularly described,” he said according to Bloomberg. “That’s why everybody wants their money back: They’re starting to realize they might be the bag-holder.”

Gundlach took issue with private credit firms calling their funds “semi-liquid” in nature. “Semi-liquid is kind of a diabolical name,” Gundlach said. “Half the time it’s liquid. It’s liquid when you don’t want your money, and it’s illiquid when you do want your money.” A little bit like "half cash, half stock", in the parlance of our times.

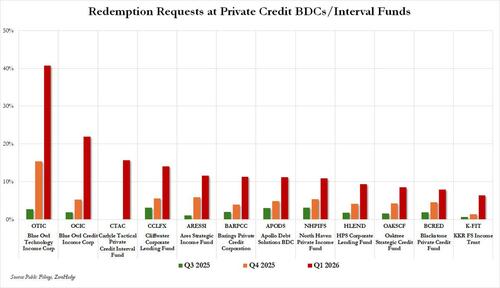

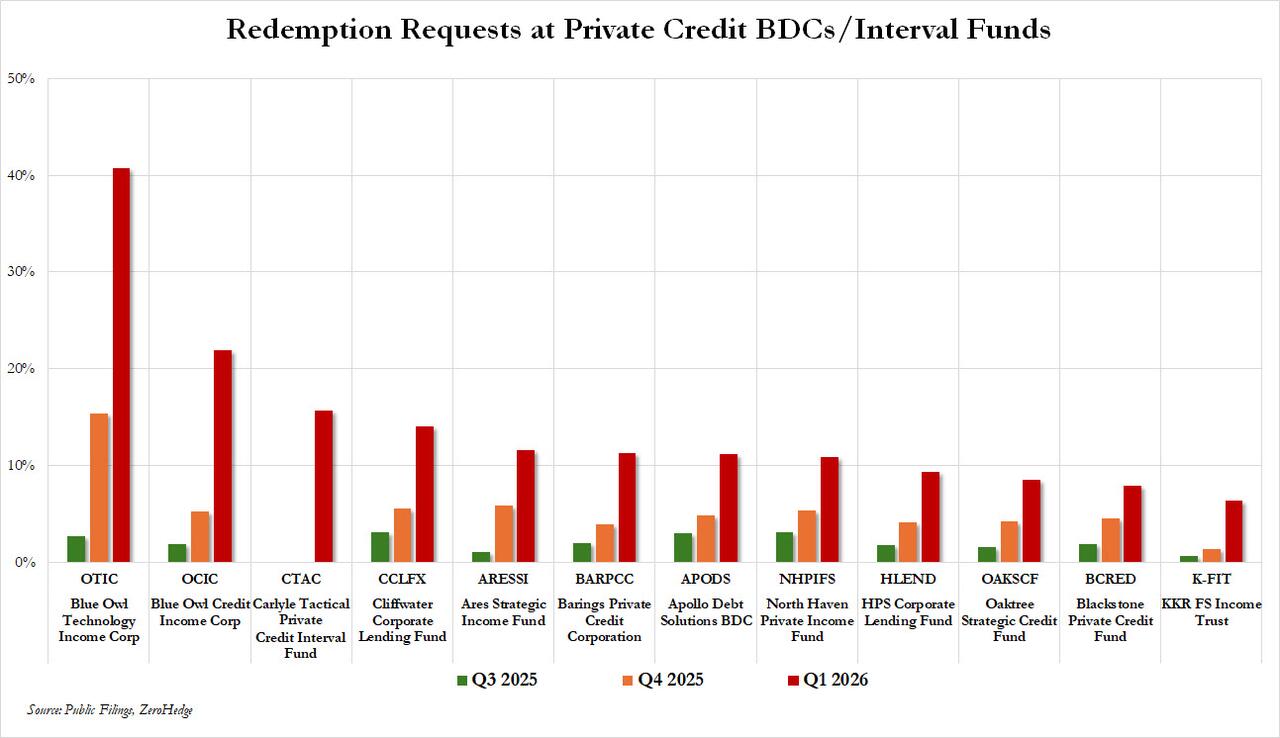

As documented extensively, private credit firms have been slammed with a wave of redemption requests, a jolt to an industry that had viewed retail investors as a new source of capital to complement institutions; instead it is scrambling to gate them as they seek their money back as cracks have emerged in the private credit architecture. At Milken and elsewhere, asset managers are now questioning the wisdom - or at least, the marketing message - of selling illiquid investments to the masses.

Gundlach also compared today’s private credit market to the boom-and-bust cycles in the dot-com era and in mortgage-backed securities and other derivatives. Risky credit might be able to hide in the private market, he said, noting that the quality in the high-yield public market is much better than it was before the global financial crisis.

“This is gonna be an interesting period because the data points aren’t as frequent as they were with the dot-coms and the mortgage market,” Gundlach said. “I don’t know what systemic means, but people are going to lose money here.”

They certainly are, and today the firm at the epicenter of the private credit crisis, Blue Owl, reminded us of that when two of its private credit funds bought back $85 million of shares as volatility in technology markets and a selloff in publicly traded loans brought down their value.

The firm cut the value of its $14.1 billion technology-focused business development fund by about 5% to $16.49 a share in the three months ended March 31, according to a filing Wednesday. The value of its $15.3 billion Blue Owl Capital Corporation, fell almost 3% to $14.41 a share.

Ever a cheerful cheerleader for his struggling product, Blue Owl co-president Craig Packer said underlying credit trends remained sound for both funds. “We continue to see solid credit performance across our portfolio of durable, mission-critical businesses with many already taking steps to adapt to the evolving AI environment,” Packer said in a statement, referring to Blue Owl Technology Finance Corp.

Blue Owl noted that share buybacks had helped boost the net asset value of the funds in the quarter. At the same time, the firm which has been facing a liquidity crunch, cut the dividend at the bigger fund to 31 cents a share from 37 cents, citing an “extended period” of declining rates and lower risk premiums. The total dividend for the technology fund was flat at 40 cents.

Blue Owl, which earlier this year precipitated the crisis in the $1.8 trillion private credit market and gated redemptions at two other private credit funds when faced with an unprecedented $5.6 billion in withdrawal requests sending shares to a record low last month, on Wednesday said it had reduced the leverage at its biggest publicly traded fund, giving it flexibility to act fast when buying opportunities come up in an improving market for lenders.

Blue Owl wasn't the only one to suffer from mismarked loans. A private credit fund overseen by Apollo Global reported a quarterly loss, citing declining valuations amid market volatility and weakness in some specific deals.

MidCap Financial Investment Corp., a business development company focused on direct lending, reported a net loss per share of 30 cents, compared to a 32 cent gain for the same period a year ago, it said in a statement. Net asset value per share fell to $13.82 compared to $14.18 at the end of December, missing analyst expectations.

BDC earnings are drawing sharper scrutiny as managers grapple with exposure to software companies confronting the disruptive potential of AI. Oaktree Capital Management said this week that it cut the value of one of its private credit funds by almost 4% as the firm marked down its software assets, while Sixth Street Specialty Lending reduced its dividend and reported a decline in net asset value per share.

“Our net loss for the quarter was driven by a combination of unrealized valuation adjustments reflecting broader credit spread widening, as well as credit weakness in certain positions,” MFIC Chief Executive Officer Tanner Powell said in a statement.

Loans marked as non-accrual - typically meaning the borrower missed debt payments - climbed to about $167 million on an amortized cost basis, from $48.5 million in the same period a year ago, according to a presentation. The firm said that its software portfolio had a fair value of $327 million, accounting for about 11% of its total holdings. MidCap is “highly selective” on those investments, avoiding categories where workflows are easily automated, it said.

Meanwhile, in a sign even more pain is yet to come for the sector, Bloomberg reported that a group of banks led by JPMorgan is expected to shoulder paper losses of more than $500 million on a debt deal for software firm Qualtrics Internationa. The banks are preparing to use their own balance sheets to fund $5.3 billion of debt for Qualtrics’ acquisition of Press Ganey Forsta. That would make it the biggest “hung” deal in the leveraged finance market this year.

According to Bloomberg, the lenders decided not to launch a formal offering after pausing early discussions on the deal in March, when investors in the leveraged loan and junk-bond markets balked because of Qualtrics’ exposure to the software rout. Back then, the roughly $1.5 billion Qualtrics loan due in 2030 had fallen to about 86 cents on the dollar, down from near par levels just one month earlier. At those levels, investors would find it more attractive to buy existing debt rather than participate in a new issuance, which would also sharply push up borrowing costs for the company.

The financing effort, led by JPMorgan, was tied to Qualtrics' $6.75 billion acquisition of Press Ganey Forsta, with the package expected to include a $3.3 billion leveraged loan and another $2 billion across junk bonds or private credit.

Qualtrics, which makes online survey tools, has emerged as one of the highest-profile examples of the pain plaguing software firms at the heart of the private credit crisis, as investors reassess business models across the industry given the rapid advances in artificial intelligence.

The reason why JPMorgan capitulated on laucnhing a formal offering is because the existing term loan is currently trading at about 84 cents on the dollar, creating a hurdle too big to overcome when pricing any new deal.

Banks typically provide bridge financing commitments to support acquisitions with the intention to sell the debt on to institutional investors as part of a syndication process, and earn a fee for doing so. They try to offload the borrowings quickly - before the transaction closes - because getting stuck with the debt on their balance sheets means they can’t commit that capacity to new deals.

In the case of Qualtrics, the company imploded much faster than anyone had expected, stiffing the bank syndicate with massive paper losses.

Qualtrics’ acquisition of Press Ganey, an online survey and data analytics business, is expected to close as soon as this month. Banks are discussing a number of potential structural changes with PE sponsor Silver Lake to make the deal more palatable to investors, and plan to bring the debt offering to the market at a later date, arguably in hopes that the current market euphoria lasts long enough to find a new, naive batch of buyers who would be willing to take on the banks' balance sheet risk. Should that happen, it’s possible that some of the paper losses banks will have to book when funding the Qualtrics deal will be reversed once they bring the transaction back to market.

Qualtrics is the biggest deal to have run into trouble this year. In February, a Deutsche Bank-led group was unable to sell about $1.2 billion of loans supporting an acquisition by Thoma Bravo-backed Conga Corp., another software business. More recently, banks led by UBS financed the tie-up of two logistics firms after pausing early talks to offload a $765 million loan to investors.

And as more and more firms reveal just how badly they mismarked their books over the years in hopes of attracting retail investors with mark-to-model gains which have in retrospect turned out to be fictitious, some are taking proactive steps to restore confidence in the space. Apollo is one of them: the alternative asset manager plans to offer investors daily valuations for its private-credit funds by the end of September, a move that could help ease worries about the health of an opaque world of lending.

The private-market giant disclosed its plans Wednesday during a call with analysts after reporting its first-quarter results.

“This is the beginning of standardization across this marketplace,” Chief Executive Marc Rowan said on the call reported by the WSJ.

Since most private investment funds provide valuations of their assets to investors on a quarterly basis, the investing public has to wait at least three months to get an updated sense of how the portfolio is performing. The marks (or valuations) are used to calculate fees and give investors a sense of their unrealized returns. Unlike with stocks or public debt, investors don’t have real-time updates on how their investments are faring.

Rowan said the firm would observe other trades, comparable assets and market trends to produce a price for assets. Then again, if all Apollo does is merely spew out what some excel model thinks the loan book is worth daily instead of every three months, nothing at all will change unless the actual marking process is also fixed.

Tyler Durden

Thu, 05/07/2026 - 06:55

Recent comments