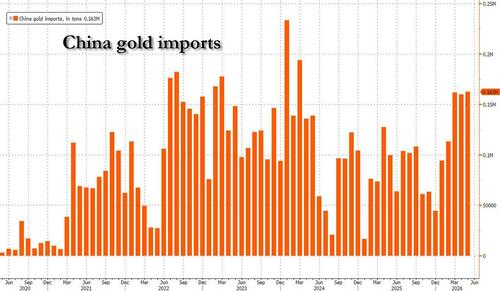

China Gold Imports Soar To Two Year High, As Hong Kong Gold Bar Imports Surge Ahead Of Clearing System Launch

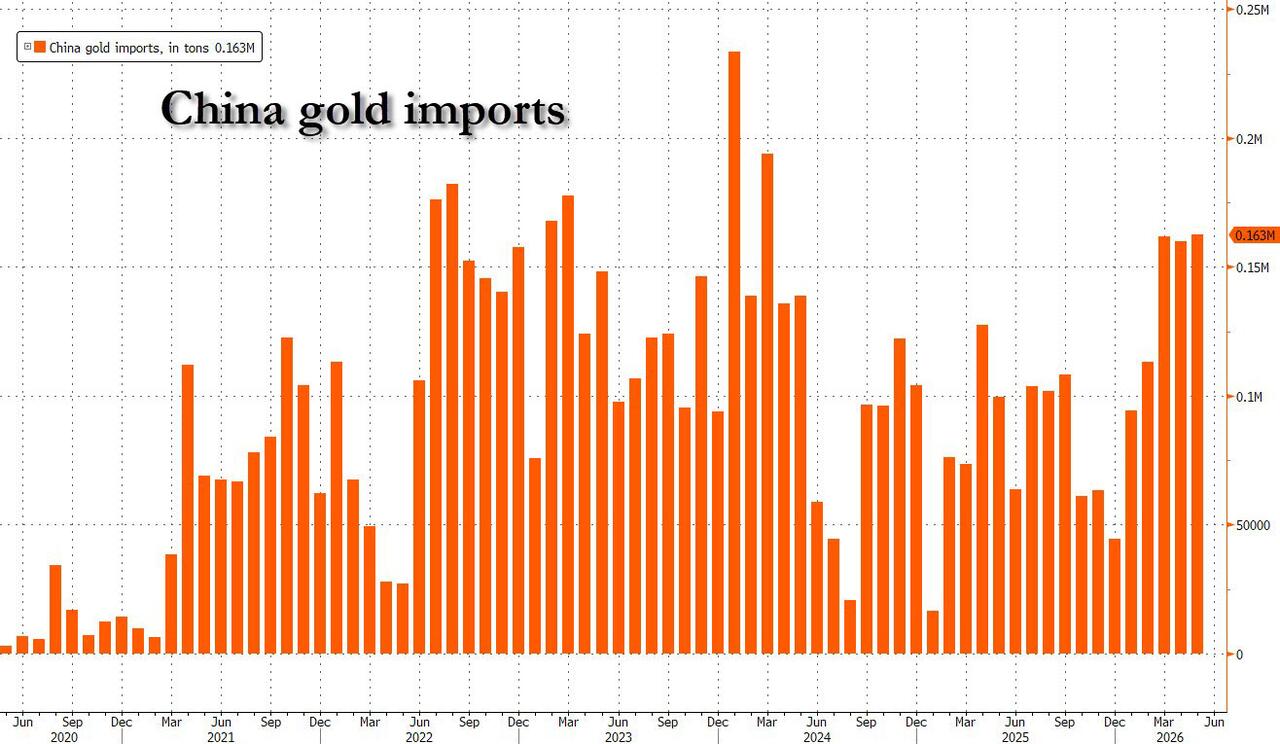

China’s monthly gold imports reached their highest in more than two years in May, showing the world’s biggest buyer’s appetite for bullion remained resilient as prices remained under pressure; the number prompted some to scratch their heads as to where all this gold is going in light of tepid official central bank purchases, coupled with the lowest gold withdrawals from the Shanghai Gold Exchange since the covid outbreak.

As Bloomberg reports, imports were around 163 tons last month, the highest since March 2024, according to customs data released on Saturday. Volumes for the first five months of 2026 were about 692 tons, up by about 76% from a year earlier.

Chinese demand for physical bullion bars, as well as metal linked to gold accumulation plans (low-barrier products that allow investors to buy gold incrementally), have been among the main drivers of the surge, said Song Jiangzhen, a researcher at the Guangzhou Southern Gold Market Academy.

China also started implementing a new import licensing regime for gold from June 1, with certain banks facing fewer restrictions. But the change may have prompted some banks to use up their existing quotas before the new system began, Song said.

Curiously, in its latest official monthly update, China's central banb, the People’s Bank of China (PBoC) only increased its gold reserves by nearly 10 tonnes last month, its 19th consecutive month of bullion purchases. The State Administration of Foreign Exchange (SAFE) announced on Sunday that China's official gold reserves rose by 320,000 troy ounces or 9.95 tonnes in May to a total of 74.96 million troy ounces or 2331.52 tonnes.

China's total foreign exchange reserves rose to $3.4422 trillion at the end of May, increasing by $31.7 billion or 0.93% from April. This is the highest level for China’s FX reserves since November 2015; they have remained above $3.3 trillion for the past 10 months.

SAFE attributed the growth of reserves to a number of factors, including a firmer US Dollar Index and rising global asset prices, adding that China's sound economic momentum has underpinned the stability of its reserves.

Experts have noted that China's rising foreign exchange reserves are closely linked to the country’s export performance. China's total foreign trade in the first four months of 2026 rose to $2.39 trillion, an increase of 14.9% year-on-year, with exports rising by 11.3% percent to $1.37 trillion and imports rising 20% percent to $1.01 trillion, according to the latest data from China's General Administration of Customs

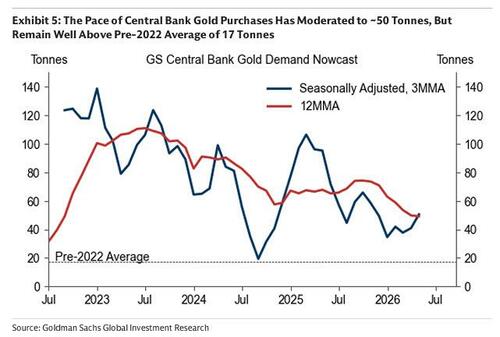

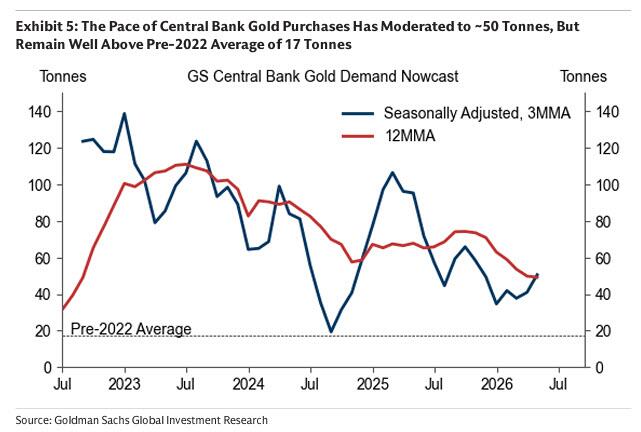

According to the latest central bank gold purchase tracker from Goldman, of the 59 tonnes of gold purchased by central bank in April, China's PBOC was estimated to have bought 24 tonnes of gold, or well below the recent pace of imports which are about 5x greater. While the pace of central bank gold purchases has moderated to ~50 tonnes/month on a 3-month (seasonally adjusted) and 12-month moving average basis, Goldman views the ongoing diversification trend as structural.

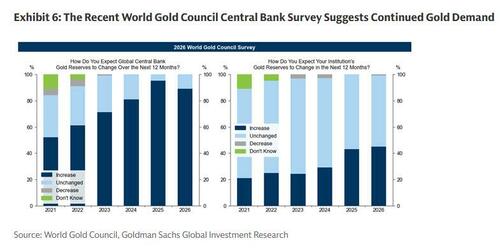

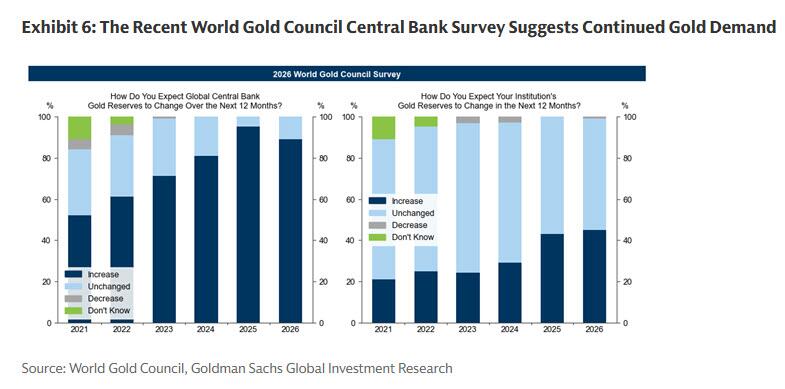

Goldman remains bullish on gold, with continued central bank diversification the main structural driver of the bank's constructive base case for gold prices, contributing 9% to its forecast for appreciation by Dec26. As we highlighted last week, a recent World Gold Council survey supports Goldman's optimistic view: a record 45% of the 76 central banks surveyed between February and May expect to increase their own gold reserves over the next 12 months, while ~90% expect global reserves to rise with the remainder expecting broadly stable holdings. As a result, Goldman assumes continued central bank accumulation of 50t/month in 2026 and 40t/month in 2027.

Meanwhile, as Kitco notes, China’s domestic gold market has shown definite signs of cooling in recent weeks.

“Amid heightened market uncertainty, gold ETFs have seen an overall reduction in assets under management, with several funds experiencing significant net outflows,” noted a report from Gelonghui Finance. “As of June 3, 14 gold ETFs recorded combined net outflows exceeding RMB 10 billion [$1.48 billion] over the past month.”

“The previously widely accepted investment view of 'buying on dips amid falling gold prices' has started to face divergence under current volatile market conditions,” they added.

Gold prices have retreated by about a quarter from the record highs reached in January, weighed down by EM selling (most notably Turkey in the early days of the Iran war), and global inflation fears amid the war in the Middle East which have pushed the US dollar sharply higher. While strong buying from Chinese consumers was a key catalyst for the January frenzy, domestic demand has since moderated, but without a major slump.

Adding to the mathematical mystery, the latest numbers from the Shanghai Gold Exchange (SGE) showed that gold withdrawals in May totaled only 63.5 tonnes – the lowest level since February of 2020 during the first wave of the COVID-19 outbreak, and around half of what they were in March of this year. Industry professionals told Gelonghui Finance that “while short-term gold price volatility may persist, the core rationale supporting gold’s strategic allocation value remains intact over the medium to long term.”

In other words, there appears to be a gap between near record imports, tepid official central bank demand, and muted gold withdrawals from the SGE.

This is not a new development: as we documented previously, China is well known for indicating just modest central bank purchases, even as total Chinese purchases of gold on the London OTC market are orders of magnitude higher.

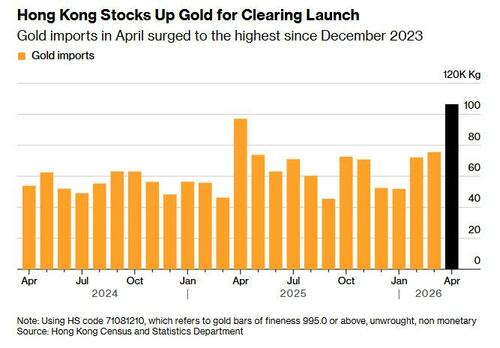

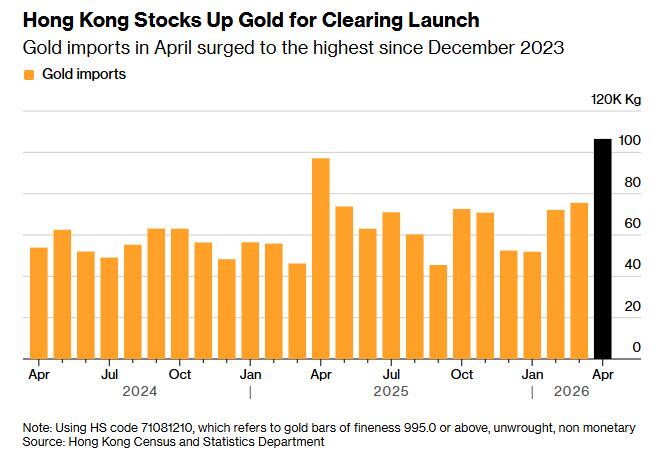

Separately, Bloomberg also reported that at least four of the 11 banks participating in Hong Kong’s new gold clearing system are importing large bullion bars in preparation for the mechanism’s planned launch in July.

Traders are receiving orders from some of the clearing banks to move 400-ounce gold bars into the city, Bloomberg reported citing people familiar with the matter. The bars meet the London Good Delivery industry standard.

The 400-ounce bars are typically traded by banks and sovereign entities in London, the world’s largest bullion trading hub, but are less common in the Asian market, which is dominated by much smaller kilobars. The banks need to build up inventories to allow for physical delivery when clearing begins next month.

By launching its gold clearing system, Hong Kong is securing first-mover advantage in a push to become Asia’s preeminent hub for bullion trading. Last week, Singapore announced its own plans to launch a clearing mechanism by the end of the year.

Both cities are aiming to capitalize on strong demand in Asia, where many investors remain bullish about the long-term prospects for the precious metal as an alternative store of wealth despite the recent drop in price as the war in the Middle East fanned concerns around inflation and higher interest rates.

In an emailed response to questions, a spokesperson for the government agency behind the system, known as the Financial Services and the Treasury Bureau, said the clearing company had been “working closely with the market to formulate the framework and rules of the clearing system” and that preparatory work had entered its final stage.

Eleven banks are on the board of the Hong Kong Precious Metals Central Clearing Company. Some of these lenders will become clearing banks from the launch, whereas others will take longer to build up their bullion capacity. While Hong Kong plans to start by using the London Good Delivery standard, its future plans are still to be decided, the people said.

In Singapore, the clearing system will be aligned with the London Good Delivery framework for large bars, as well as delivery and settlement standards for kilobars adopted by major exchanges in Chicago and Shanghai.

Tyler Durden

Mon, 06/22/2026 - 18:50

via CNN

via CNN

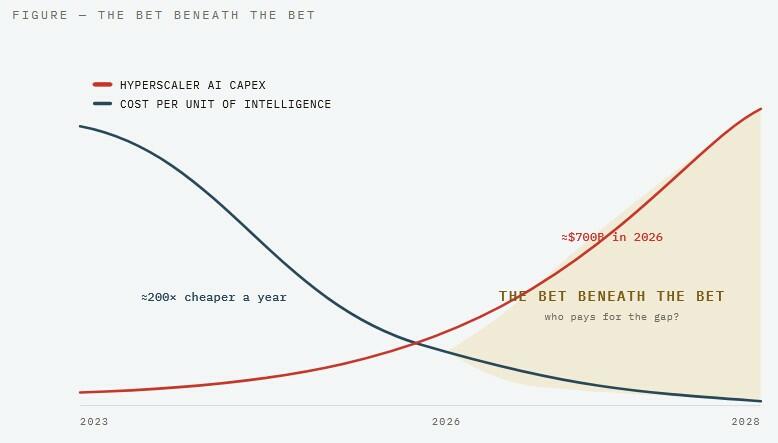

Illustrative. Trend directions are schematic; the figures are point estimates drawn from 2026 hyperscaler capex guidance (~$700B) and reported per-token inference-price declines (~200× per year). Not a fitted data series.

Illustrative. Trend directions are schematic; the figures are point estimates drawn from 2026 hyperscaler capex guidance (~$700B) and reported per-token inference-price declines (~200× per year). Not a fitted data series.

Image source: Astra

Image source: Astra A person receives a vaccine in Los Angeles, in this file photograph. Robyn Beck/AFP via Getty Images

A person receives a vaccine in Los Angeles, in this file photograph. Robyn Beck/AFP via Getty Images

The Lincoln Memorial Reflecting Pool is refilled after it was repaired and repainting as part of President Donald Trump's “Make the District of Columbia Safe and Beautiful” initiative ahead of America's 250th anniversary in Washington on June 4, 2026. Madalina Kilroy/The Epoch Times

The Lincoln Memorial Reflecting Pool is refilled after it was repaired and repainting as part of President Donald Trump's “Make the District of Columbia Safe and Beautiful” initiative ahead of America's 250th anniversary in Washington on June 4, 2026. Madalina Kilroy/The Epoch Times

Recent comments